11 Ways to Finance Commercial Real Estate Energy Retrofits

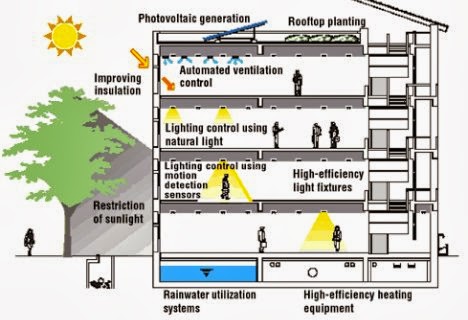

According to the U.S. Department of Energy, commercial buildings account for 35 percent of U.S. (and 40 percent of global) electricity consumption. Most commercial real estate professionals accept that energy efficient buildings can, and do, impact the value of the underlying asset. Notwithstanding this recognition, existing commercial buildings on average spend 30 percent of their budgets on operating costs and account for close to 20 percent of all global carbon emissions.

While they understand the benefits, the challenge for most commercial real estate owners and operators is not whether to implement energy efficient retrofits, but rather how to pay for or finance such improvements.

While they understand the benefits, the challenge for most commercial real estate owners and operators is not whether to implement energy efficient retrofits, but rather how to pay for or finance such improvements.

The following list is a basic primer of ways to finance these types of retrofits in commercial real estate space. It is not intended to be fully inclusive and does not discuss the benefits or drawbacks (and there are many) of each financing structure. But it does offer an introduction to a topic that has become, and will continue to be, of critical importance to the commercial real estate industry.

1. Capital Expenditure Financing. Due largely to the lack of consistent alternative funding sources, most energy retrofits to date are financed through the cash flow, reserves, capital raises, or reallocation of internal funds from the property owner.

2. Debt Financing. Both secured and balance sheet debt financing through commercial banks, credit unions, and other types of lenders is available in limited instances, and for limited borrowers. Debt financing from federal and state sources is also provided through a variety of state or local programs. A few examples of these programs include federal legislation such as The American Reinvestment Act of 2009, President Obama’s Better Building Initiative, and Small Business Administration loan programs, as well as state or local revolving funds such as the Green Jobs-Green New York Program administered by the New York State Energy Research and Development Authority. Program-related investments through non-profit organizations, such as the MacArthur Foundation, structured as low interest bridge or subordinated loans or loan guarantees are often leveraged through community development financial institutions to secure funding for energy efficiency projects.

3. Bond Financing. While not widely used, some experts have suggested that private corporate or municipal bonds, such as the Federal Qualified Energy Conservation Bonds and the CDFI Bond Guarantee Program, are a feasible structure for scaling large efficiency retrofits through the creation of funds or special purpose entities designed to finance multiple smaller transactions.

4. PACE Financing. If and when authorized by state law, Property Assessed Clean Energy Programs are a form of tax lien financing that allow owners to borrow from local government sources (16 currently in the U.S.) or private investors through a private placement. The loans are typically repaid through long-term special assessments up to 30 years, levied against the borrower’s property tax bills.

5. On-Bill Financing. This financing structure utilizes funds provided by third-party capital sources and a repayment procedure administered by local utilities. Specifically, the borrower repays the loan over a short term (typically not exceeding 36 months) through a supplemental charge on the owner’s utility bill.

6. Sustainable Energy Utility Financing. There are a small number of sustainable energy utilities throughout the U.S. -- for example, the Cambridge Energy Alliance -- that are created by state or local municipalities for the purpose of providing or arranging project financing and facilitating public-private partnerships to foster energy efficient and renewable energy-related development.

7. ESCO Financing. Under this structure, an energy service company enters into long-term contracts with owners to design, construct, and often finance the retrofit project. In turn, the ESCO is repaid through a shared savings, guaranteed savings, or performance contracting model. With a typical performance contract, an ESCO assumes some portion of the risk over a retrofit project’s useful life by offering a guaranty of energy.

8. Energy Service Agreements/Performance Contracts. Energy service agreements and performance contracts expand the traditional ESCO model through third-party ownership, management, and maintenance of the installed efficiency equipment. This eliminates the owner’s initial capital costs, which can be substantial, and allows the owner to simply make scheduled payments to the energy efficiency firm, such as Metrus Energy and CalCEF, typically based upon the level of energy savings as operating expenditures for the asset.

9. Utility Financing. While differing in form and substance, many utilities offer financial incentives, rebates, grants, and loans for energy retrofits. Typically, the loans are repaid through an on-bill structure underwritten and administered by the utility.

10. Tax Credits and Incentives. Often used in conjunction with other financing tools, federal and state governments offer tax incentives (including credits, grants, and rebates) to encourage owners and operators to make capital investments into energy efficiency retrofits.

11. Equipment Leases. While not conducive for deep or large-scale retrofit projects, leasing of energy efficient equipment allows owners to reduce or largely eliminate upfront capital costs through lease and lease purchase agreements that can be structured as either capital or operating leases.

The foregoing summary is only the beginning. A commercial real estate owner should not only assess the values, challenges, and risks of each financing structure with the economic realities of a particular asset, the owner must also seek the input of professional advisers to assist in navigating the opportunities and potential pitfalls.

Source: CCIM.com, Michael C. Polentz is co-chair of the Real Estate & Land Use Practice Group at Manatt, Phelps & Phillips, LLP, located in the Palo Alto, CA.

The following list is a basic primer of ways to finance these types of retrofits in commercial real estate space. It is not intended to be fully inclusive and does not discuss the benefits or drawbacks (and there are many) of each financing structure. But it does offer an introduction to a topic that has become, and will continue to be, of critical importance to the commercial real estate industry.

1. Capital Expenditure Financing. Due largely to the lack of consistent alternative funding sources, most energy retrofits to date are financed through the cash flow, reserves, capital raises, or reallocation of internal funds from the property owner.

2. Debt Financing. Both secured and balance sheet debt financing through commercial banks, credit unions, and other types of lenders is available in limited instances, and for limited borrowers. Debt financing from federal and state sources is also provided through a variety of state or local programs. A few examples of these programs include federal legislation such as The American Reinvestment Act of 2009, President Obama’s Better Building Initiative, and Small Business Administration loan programs, as well as state or local revolving funds such as the Green Jobs-Green New York Program administered by the New York State Energy Research and Development Authority. Program-related investments through non-profit organizations, such as the MacArthur Foundation, structured as low interest bridge or subordinated loans or loan guarantees are often leveraged through community development financial institutions to secure funding for energy efficiency projects.

3. Bond Financing. While not widely used, some experts have suggested that private corporate or municipal bonds, such as the Federal Qualified Energy Conservation Bonds and the CDFI Bond Guarantee Program, are a feasible structure for scaling large efficiency retrofits through the creation of funds or special purpose entities designed to finance multiple smaller transactions.

4. PACE Financing. If and when authorized by state law, Property Assessed Clean Energy Programs are a form of tax lien financing that allow owners to borrow from local government sources (16 currently in the U.S.) or private investors through a private placement. The loans are typically repaid through long-term special assessments up to 30 years, levied against the borrower’s property tax bills.

5. On-Bill Financing. This financing structure utilizes funds provided by third-party capital sources and a repayment procedure administered by local utilities. Specifically, the borrower repays the loan over a short term (typically not exceeding 36 months) through a supplemental charge on the owner’s utility bill.

6. Sustainable Energy Utility Financing. There are a small number of sustainable energy utilities throughout the U.S. -- for example, the Cambridge Energy Alliance -- that are created by state or local municipalities for the purpose of providing or arranging project financing and facilitating public-private partnerships to foster energy efficient and renewable energy-related development.

7. ESCO Financing. Under this structure, an energy service company enters into long-term contracts with owners to design, construct, and often finance the retrofit project. In turn, the ESCO is repaid through a shared savings, guaranteed savings, or performance contracting model. With a typical performance contract, an ESCO assumes some portion of the risk over a retrofit project’s useful life by offering a guaranty of energy.

8. Energy Service Agreements/Performance Contracts. Energy service agreements and performance contracts expand the traditional ESCO model through third-party ownership, management, and maintenance of the installed efficiency equipment. This eliminates the owner’s initial capital costs, which can be substantial, and allows the owner to simply make scheduled payments to the energy efficiency firm, such as Metrus Energy and CalCEF, typically based upon the level of energy savings as operating expenditures for the asset.

9. Utility Financing. While differing in form and substance, many utilities offer financial incentives, rebates, grants, and loans for energy retrofits. Typically, the loans are repaid through an on-bill structure underwritten and administered by the utility.

10. Tax Credits and Incentives. Often used in conjunction with other financing tools, federal and state governments offer tax incentives (including credits, grants, and rebates) to encourage owners and operators to make capital investments into energy efficiency retrofits.

11. Equipment Leases. While not conducive for deep or large-scale retrofit projects, leasing of energy efficient equipment allows owners to reduce or largely eliminate upfront capital costs through lease and lease purchase agreements that can be structured as either capital or operating leases.

The foregoing summary is only the beginning. A commercial real estate owner should not only assess the values, challenges, and risks of each financing structure with the economic realities of a particular asset, the owner must also seek the input of professional advisers to assist in navigating the opportunities and potential pitfalls.

Source: CCIM.com, Michael C. Polentz is co-chair of the Real Estate & Land Use Practice Group at Manatt, Phelps & Phillips, LLP, located in the Palo Alto, CA.

DISCLAIMER: This blog has been curated from an

alternate source and is designed for informational purposes to highlight the

commercial real estate market. It solely represents the opinion of the specific

blogger and does not necessarily represent the opinion of Pacific Coast

Commercial. www.PacificCoastCommercial.com

Keywords: San

Diego Commercial Real Estate For Sale, Commercial Property In San Diego,

Commercial Real Estate In San Diego, San Diego Investment Real Estate,

Commercial Property Management In San Diego, San Diego Commercial Property

Management, Commercial Property Management San Diego, Managed Commercial

Property San Diego, Commercial Property For Sale San Diego, San Diego

Commercial Real Estate Leasing

Comments

Post a Comment